Award-winning PDF software

form 5471 (schedule o) (rev. december 2012) - internal revenue

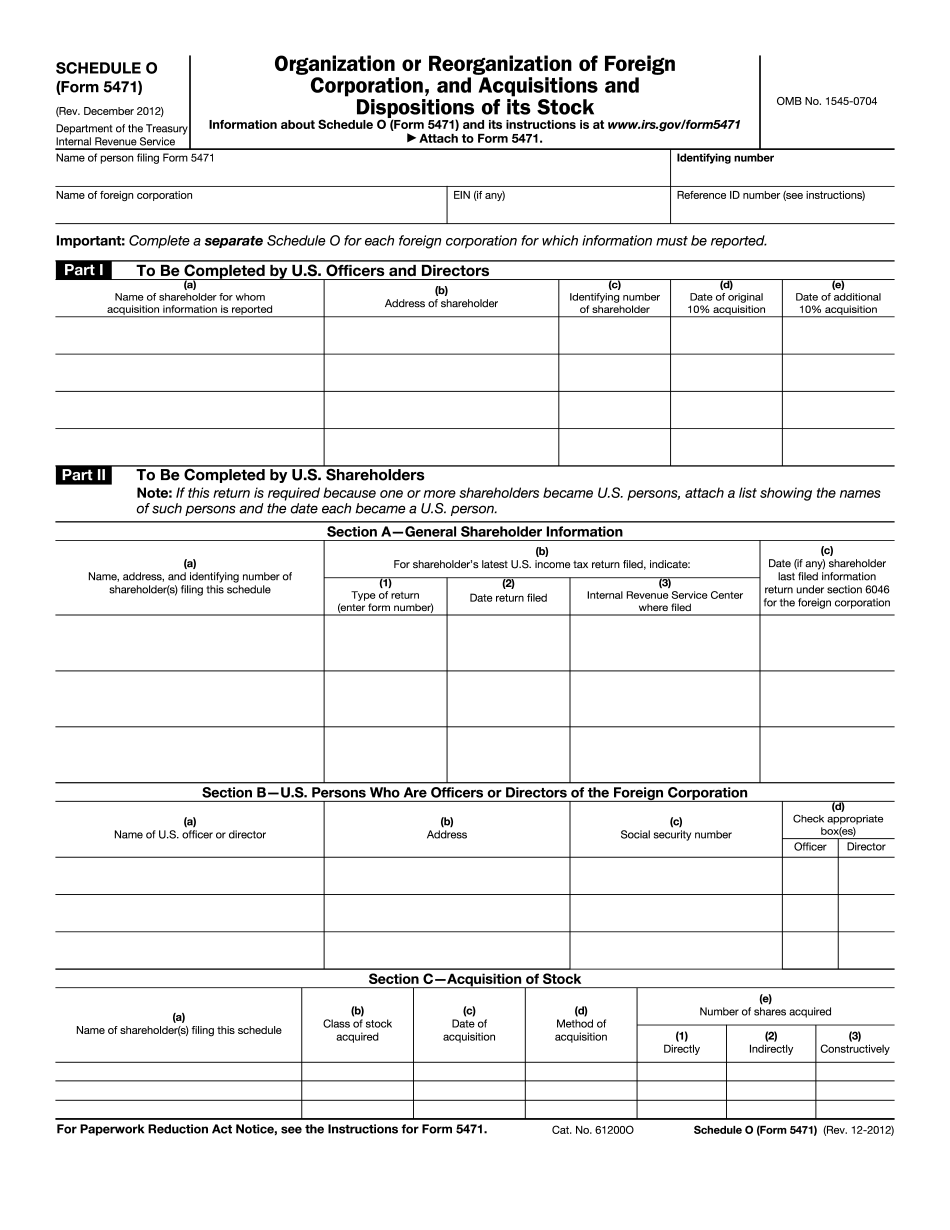

Members of the board of directors must complete this Schedule O. Part II. To Be Completed by All Other Officers and . Members of the board of directors must complete this Schedule O. Please Note: For foreign corporations: If the foreign corporation has a resident agent for service of processes, such agents shall complete this Schedule O. (Note: For foreign corporations where a resident agent cannot be located, you must also complete the Schedule R.) Part III. To Be Resubmitted as a Part 3. This part must be submitted to the Secretary for the annual report as scheduled in Part I. Complete the form and return to the office of the Department of the Treasury or Treasury Inspector General. Return the original and a copy to the Foreign Investment in Real Property Disclosure Act (FIRAS). The form must be completed by each foreign corporation with respect to which you want to report.

About form 5471, information return of us persons with respect

Filing of Form 5471. For purposes of section 6038 of the Internal Revenue Code of 1986, a nonresident alien individual who, in a tax year, files Form 5471 and schedules, and is treated as an officer, director, or employee of a corporation, will not be treated as a domestic trust under section 7879(a)(3)(C) or 8853(a)(1). For each reportable controlled entity, the Corporation, except as provided herein, must file an individual consolidated return under section 6011(b)(2)(B) by the due date of the return without regard to the due date of the return of a reportable controlled foreign corporation. Each individual controlled entity must file, as of the day before the due date of the return of the reportable controlled foreign [[Page 666]] corporation, each Schedule O, and the Schedule C on schedule O-A, Form 8802, which is filed with the return and with each other return for which the Corporation.

Demystifying the form 5471 part 6. schedule o | sf tax counsel

K for the Fiscal Year Ended June 30, 2018 9-Q for the Fiscal Year Ended June 30, 2018 10-K for the Fiscal Year Ended June 30, 2018, Annual Report for the Fiscal Year Ended June 30, 2017 9-K for the Fiscal Year Ended June 30, 2017 10-K for the Fiscal Year Ended June 30, 2017, Annual Report for the Fiscal Year Ended June 30, 2016 9-K for the Fiscal Year Ended June 30, 2016 10-K for the Fiscal Year Ended June 30, 2016 2. The Company has, through the date of this prospectus, not issued a prospectus or other offering materials except in one or more of the following circumstances: the Company has determined that it is unlawful in the United States or the home country of these purchasers to issue any such securities; the issuance of securities pursuant to this prospectus has been declared a “qualified public offering”.

How to prepare schedule o of form 5471 for stock organization

Resident of the United States at the time the corporation has become a nonresident alien is required to file Schedule O. However, Schedule O only covers a foreign corporation formed on or after January 1, 1979. For some corporations, it might be difficult to tell whether they were formed on or before or after that date. But it is usually a good idea to check the Form 15-A, if one is available for filing, for the date your corporation became foreign. The Form 15-A is a two-page form that contains a detailed description of your corporation. It is not always on file. But it is generally available if your corporation has more than fifty shareholders. If your corporation did not begin operating in the United States until after January 1, 1979, check the schedule for the corporation you formed with your spouse or common law husband to discover whether and when you.

Form 5471: basics u.s. citizens should know | h&r block

If there are additional exhibits required to be filed pursuant to 5373(b)(6), then it can be filed as a Part III entity, but that would be outside the scope of this blog. There is no time frame for the registration of this information, as the information was only made available to the public on July 9th, and as I mentioned earlier, we are only now getting into 2017. There is no deadline to file, however, once you have filed information, the IRS will take the information back and file it within 60 days, after which time it is no longer available for tax planning purposes because there is no longer a pending status. There was a lot of confusion about this issue in 2016 due to the limited timeframe, and there is a lot of confusion in 2017 as the same information is now publicly available. You should note.